15 Free Money Hacks That Put Real Cash in Your Pocket (2026)

You don't need a side hustle to put extra cash in your pocket this month. These 15 free money hacks pay you from money you're already owed and things you already do.

Disclosure: This post may contain affiliate links. As an Amazon Associate, we earn from qualifying purchases. This comes at no extra cost to you. Read our privacy policy for more information.

Want to Make Extra Money Now?

Earn up to $50 per survey with the #1 survey site.

Surveys with a $5 minimum cashout & fast payouts.

Get paid to play games, take surveys & try new apps.

Get paid for surveys, videos & shopping online.

Get paid for testing apps, games & surveys.

You don’t need a side hustle to put extra cash in your pocket this month. These 15 free money hacks pay you from money you’re already owed and things you already do.

Free money hacks are legit, repeatable moves that hand you cash for things you already do or money you are already owed.

The biggest wins are your full 401(k) match, bank and credit card sign-up bonuses, stacked cash-back apps, and unclaimed money in your name. Most take under 20 minutes.

Is “Free Money” Actually Real?

Yes, legitimate free money is real. It shows up as employer matches, bank bonuses, cash back, unclaimed property, and government programs you simply have to claim, and none of it ever charges a fee.

Free money sounds like a scam because so much of it is. Yet a huge amount of legitimate cash goes unclaimed every year simply because nobody bothers to ask for it.

I collected a little over $1,100 of it myself last year between two bank bonuses, a card bonus, and a forgotten utility deposit. None of it took more than an evening of setup.

This isn’t a budgeting lecture. Every hack below is a specific, provable way to earn rewards, unlock cash you’re entitled to, or collect money that already has your name on it.

Work the list from top to bottom. The first handful of hacks alone can be worth several thousand dollars a year.

The Best Free Money Hacks

In short, the quickest payouts come from free stock offers and cash-back app cash-outs, while unclaimed money is the biggest low-effort win.

Not every hack pays the same or takes the same effort. Use this table to decide where to start based on how fast you want the cash.

| # | Free money hack | Typical payout | Effort | Speed |

|---|---|---|---|---|

| 1 | Unclaimed money search | $50 to $5,000+ | Low | 1 to 8 weeks |

| 2 | Full 401(k) match | $1,000 to $6,000/yr | Low | Ongoing |

| 3 | Bank sign-up bonus | $100 to $400 | Medium | 60 to 90 days |

| 4 | Credit card welcome bonus | $200 to $750 | Medium | 90 days |

| 5 | Free stock offers | $5 to $200 | Low | Instant to days |

| 6 | Cash-back apps | $200 to $600/yr | Low | Ongoing |

| 7 | Class-action settlements | $10 to $500 | Low | Months |

Now let’s walk through all 15 hacks in detail, starting with the easiest ways to turn spare minutes into real cash.

1. Get Paid With Rewards and Survey Apps

Rewards and survey apps pay real cash for small pockets of downtime. Watching videos, answering questions, or searching the web all earn points.

If you’d rather skip the trial and error, start with these six. Each one has a long track record of actually paying members, and signing up takes about a minute.

| # | Survey site | Earn per survey | Sign-up bonus | Join |

|---|---|---|---|---|

| 1 | Survey Junkie | $1 to $50 | $1 | Join Now |

| 2 | Sproutful | Varies | 50 points | Join Now |

| 3 | Swagbucks | $0.25 to $4 | $5 | Join Now |

| 4 | Freecash | Varies | $10 | Join Now |

| 5 | Branded Surveys | $0.50 to $2.50 | 100 points | Join Now |

| 6 | YouGov | $0.50 to $1 | $2 | Join Now |

Survey Junkie and Swagbucks pay for surveys and micro-tasks, Freecash adds paid app and game testing, and Sproutful keeps things simple with quick surveys and a low $5 cashout. None will replace a paycheck, but they turn idle minutes into gift cards and PayPal cash.

The trick is stacking easy, passive earnings rather than grinding low-value tasks for pennies. Focus on the highest-paying surveys and simple daily point streaks.

Keep one app open during TV time and let the passive points build in the background. Cashing out monthly keeps the rewards feeling worthwhile.

Sticking to the highest-paying survey sites keeps your time worth the effort and filters out the ones that barely pay.

Realistically, most people pull in $20 to $100 a month here, not a full-time paycheck. Treat it as coffee money that quietly stacks up while you’re only half-watching TV.

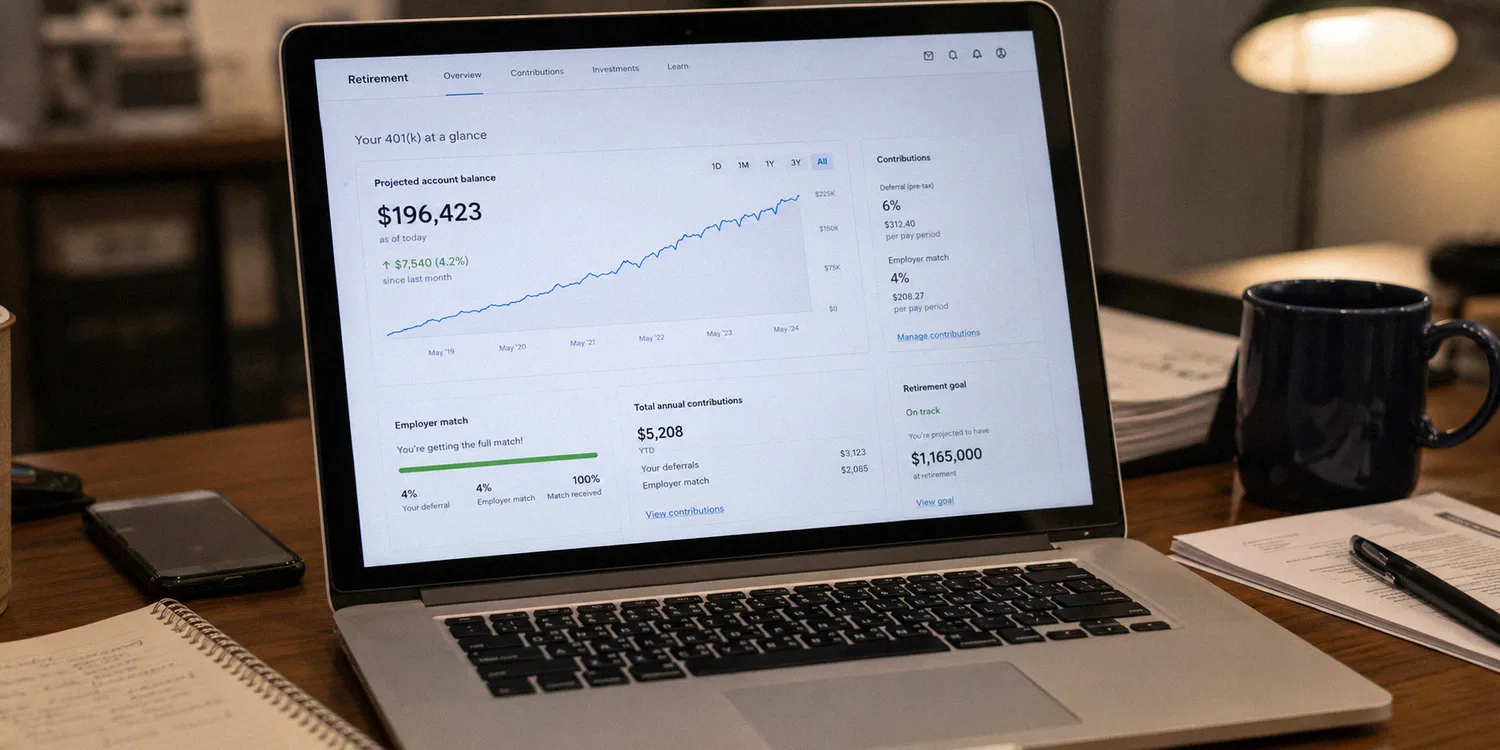

2. Claim Your Full Employer 401(k) Match

An employer 401(k) match is the closest thing to guaranteed free money that exists. You lock in an instant 50% to 100% return the moment you contribute a dollar.

A common setup matches 100% of the first 3% to 6% of your pay. On a $55,000 salary, a full 6% match is $3,300 in free money every single year.

Log into your retirement portal and confirm you’re contributing enough to capture the entire match. Anything less is quietly turning down part of your paycheck.

If cash is tight, fund the match before any other savings goal on your list. No cash-back app here can compete with a dollar-for-dollar return that also grows tax-deferred.

Reset your contribution percentage after every raise, too. Bumping it by even 1% a year keeps your free match climbing without you feeling the pinch.

Keep an eye on the vesting schedule, since some employers only let you keep the match after a few years on the job. Your own contributions, though, are always yours to take when you leave.

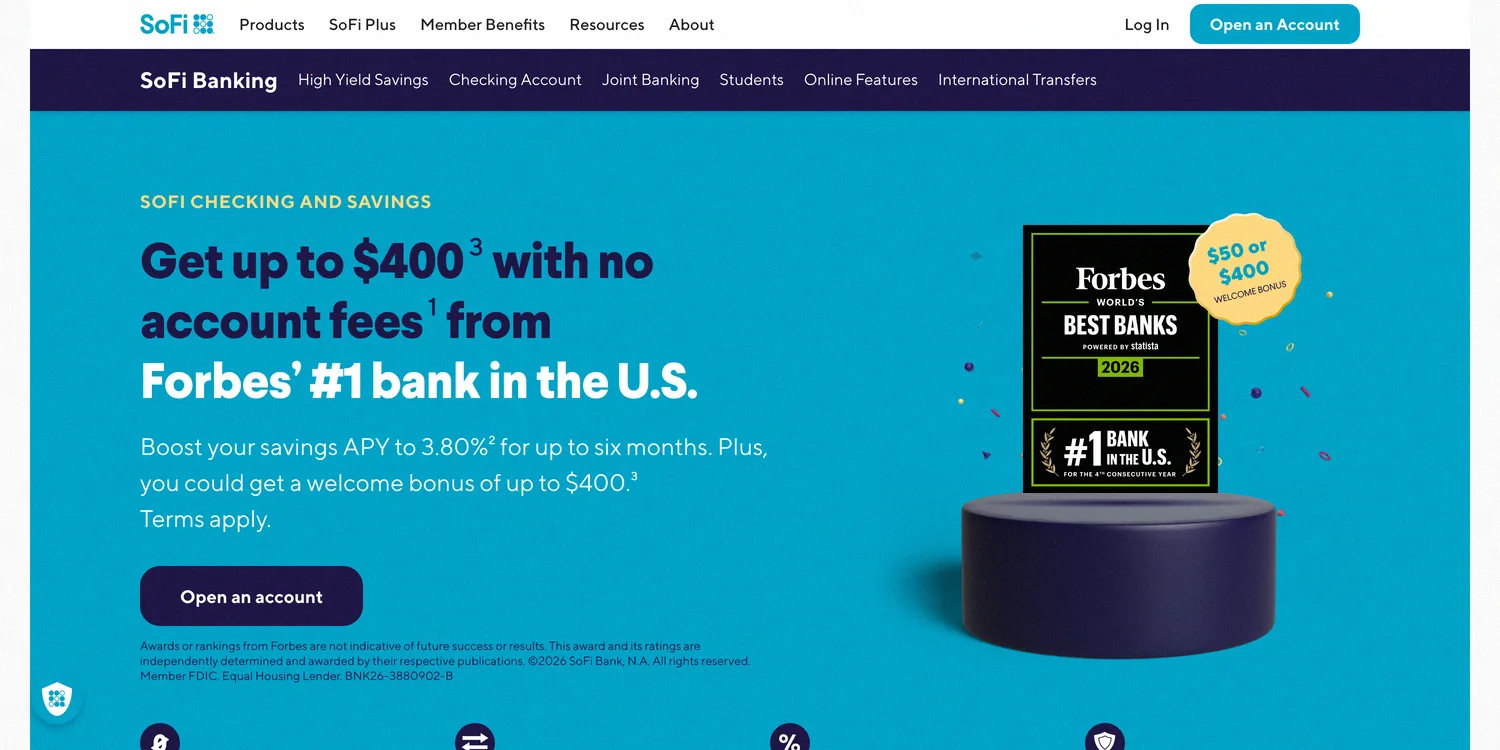

3. Grab Bank Account Sign-Up Bonuses

Banks pay $100 to $400 just for opening an account and meeting a few simple terms. They want your deposits, and they are willing to pay real cash to win you over.

Most bonuses require a direct deposit or a minimum balance held for 60 to 90 days. Once the cash posts to your account, you’re free to move on to the next offer.

The last checking bonus I claimed paid me $300 about six weeks after my first direct deposit hit. The application itself took maybe ten minutes on a Sunday morning.

Chase, SoFi, and Capital One run these promotions constantly, and comparison sites track the current highest payouts. Set a calendar reminder for each qualifying deadline so a bonus never slips away.

Keep a simple spreadsheet of which bonuses you have claimed and when. Some banks let you earn again after a year or two, so an old offer can quietly become new money.

New promotions rotate constantly, and the highest-paying sign-up bonus apps will pay you $50 or more just to open an account.

One heads-up: these bonuses count as taxable interest, so a 1099-INT form will show up in January. It’s still free money, so just report it and keep going.

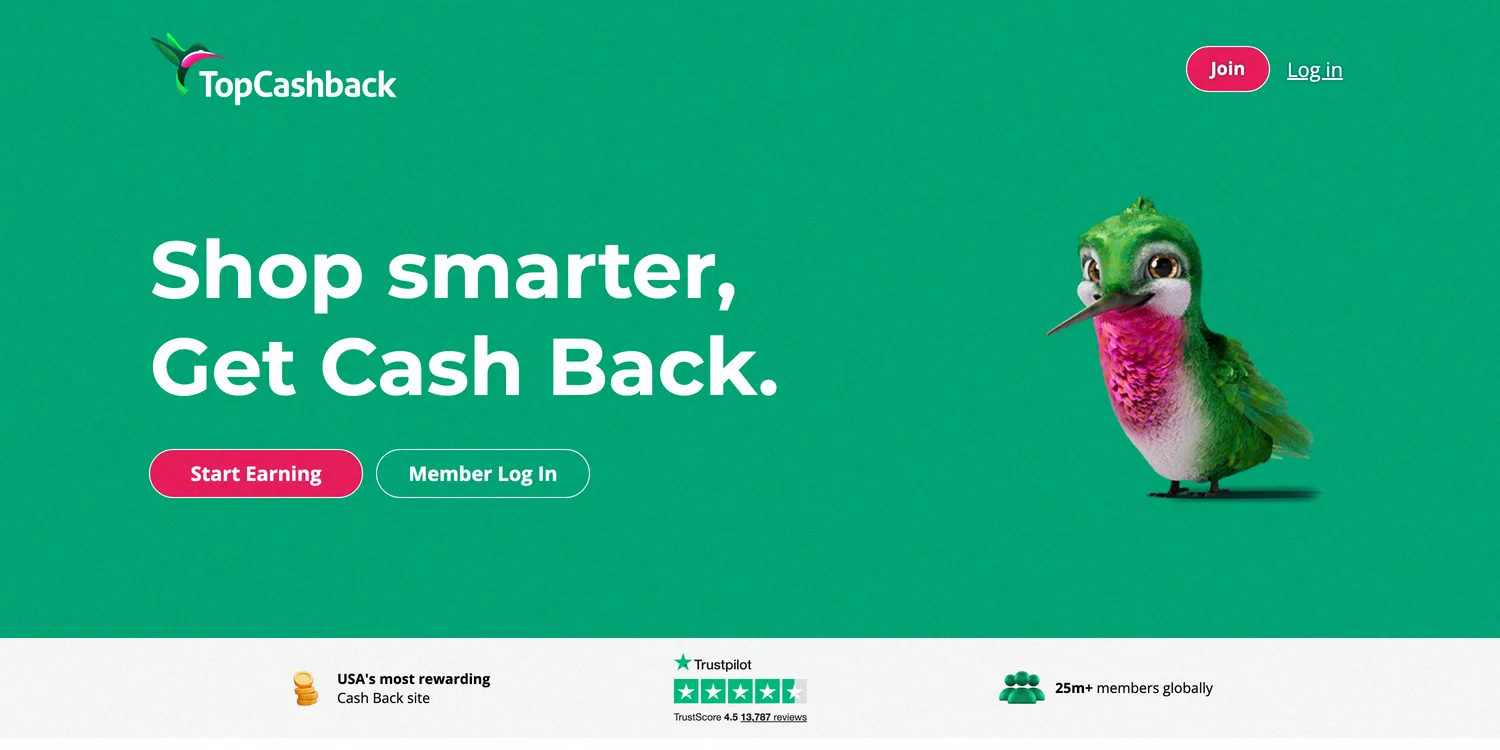

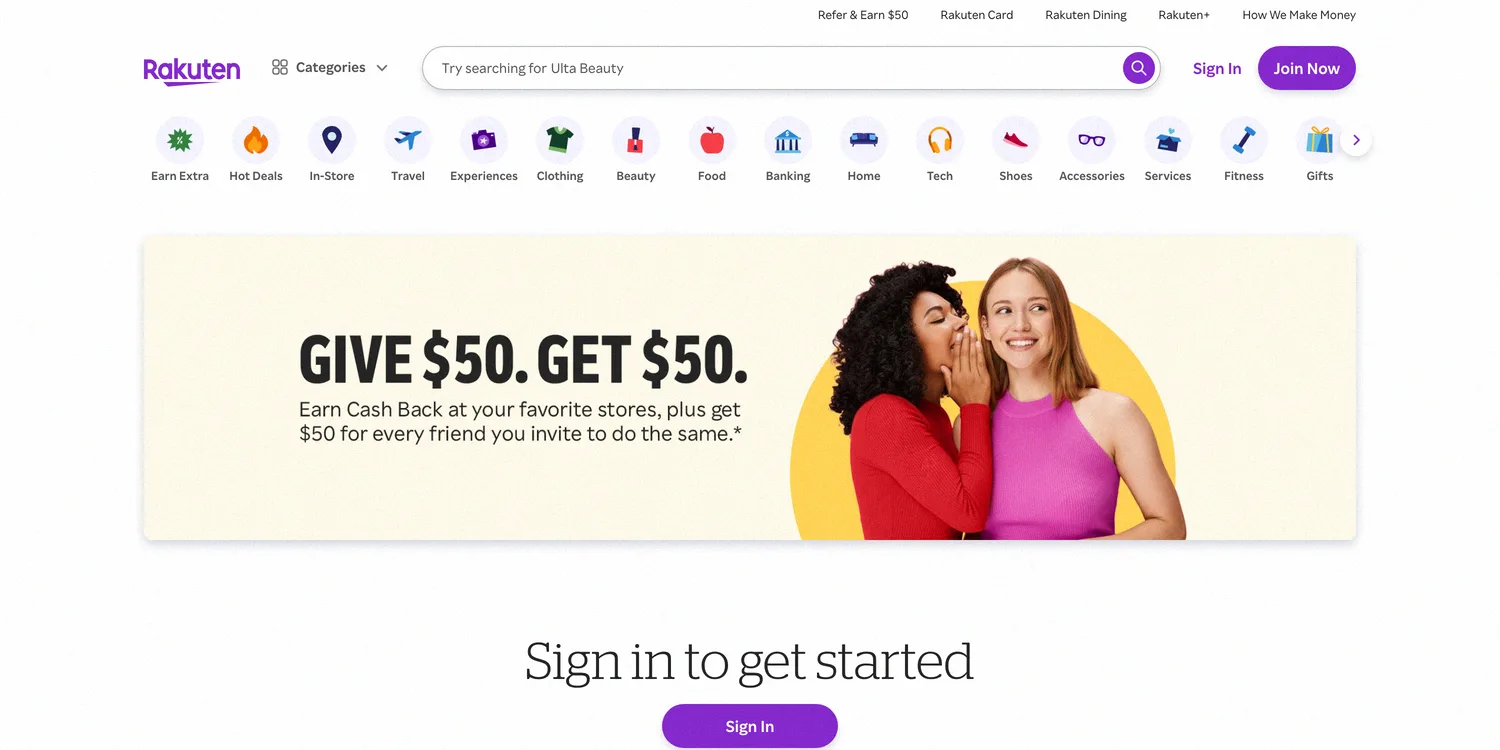

4. Stack Cash-Back Apps on Everyday Spending

Cash-back apps refund a slice of money you were going to spend anyway. Groceries, gas, and online orders all turn into quiet little rebates.

These five cover just about every kind of spending, from online orders to groceries and gas. All of them are free to join.

| # | Cash-back app | Best for | Sign-up bonus | Join |

|---|---|---|---|---|

| 1 | TopCashback | Highest online rates | $10 | Join Now |

| 2 | Rakuten | Big-name online stores | Varies | Join Now |

| 3 | BeFrugal | Up to 40% back | $10 | Join Now |

| 4 | Fetch Rewards | Any receipt | $1.50 with code | Join Now |

| 5 | Upside | Gas fill-ups | Varies | Join Now |

Rakuten pays cash back at thousands of online stores, while Fetch Rewards pays points on every receipt you scan. Running both at once means you often get paid twice on the exact same purchase.

The real power is stacking a cash-back app on top of a rewards credit card and a store sale. A single order can layer three separate savings without any extra work.

Payouts arrive by PayPal, direct deposit, or gift card once you clear a small threshold. The best cash-back shopping apps can quietly return a few hundred dollars over a year of normal spending.

Rates swing from around 1% at big retailers to 10% or more during seasonal promotions. A quick glance at the app before checkout turns a routine order into a small rebate.

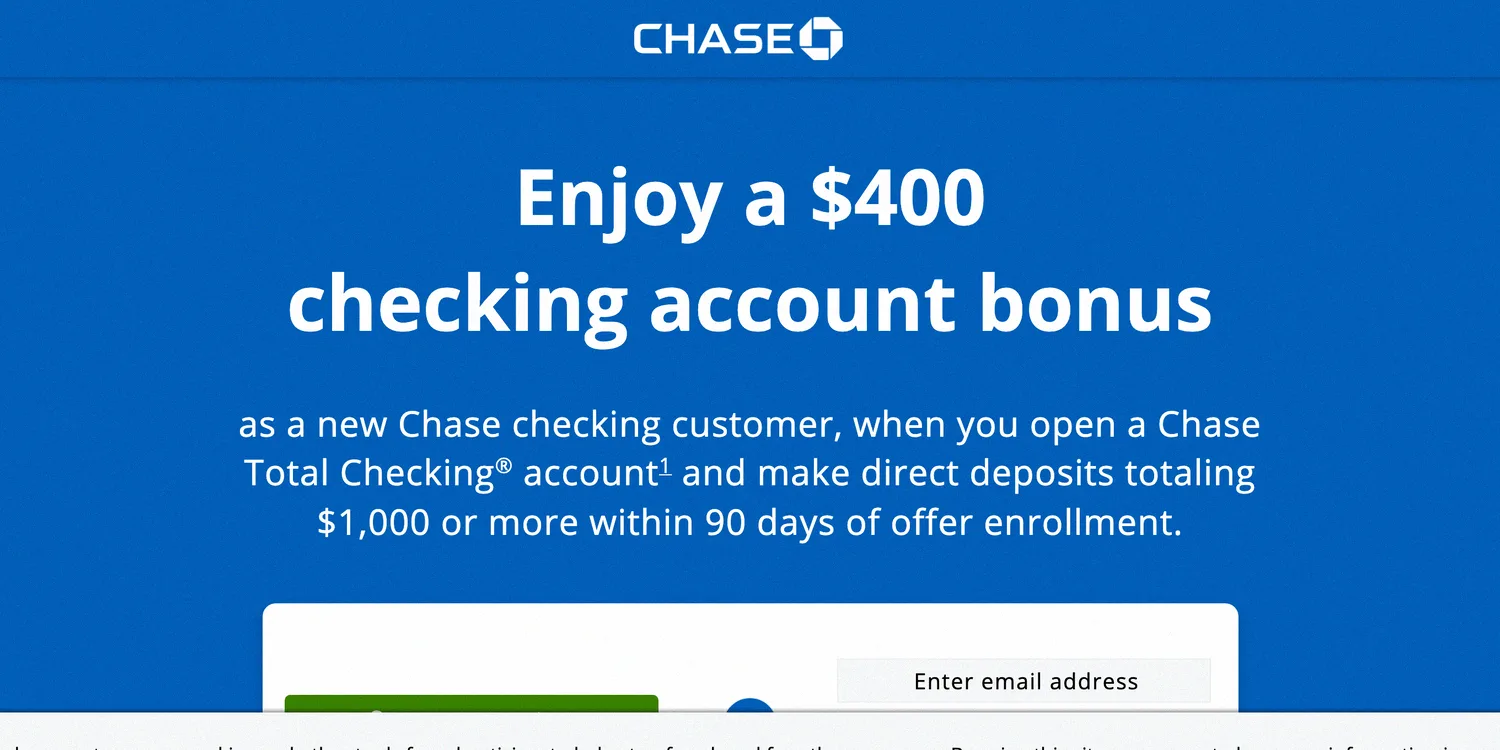

5. Collect Credit Card Welcome Bonuses

A credit card welcome bonus can hand you $200 to $750 for spending you already planned. Card issuers pay big to earn a permanent spot in your wallet.

Most bonuses ask you to spend a set amount within the first three months. If that lines up with normal expenses like bills and groceries, the reward is essentially free.

The one rule that makes this work is paying the full statement balance every month. Carry a balance and interest charges will wipe out the bonus fast.

Time a new card to a big planned purchase, like a flight or an annual insurance bill. Meeting the spend requirement becomes effortless when the money was leaving your account anyway.

This hack only pays if you already manage credit responsibly. If a card tempts you to overspend, skip it and stick to the debit-based hacks on this list.

6. Get Free Stock From Brokerage Sign-Ups

Investing apps give away free shares of stock just for opening an account. It’s a marketing giveaway that can quietly turn into real, growing money.

Moomoo and Public regularly hand new users a free share worth anywhere from a few dollars to a couple hundred. Referring a friend often unlocks a second free share for both of you.

Fund the account with the minimum required, claim your share, and simply let it sit. You’re under no obligation to trade or add another cent after that.

Read the terms first, though, since some offers need the account to stay open for a set period. Close it early and you can forfeit the share you just earned.

The share is usually pulled at random from a set list, so think of it like a scratch-off ticket. Sell it or hold it, but either way your account grew for free.

7. Redeem Receipt-Scanning App Rewards

Some apps pay you simply for photographing receipts you would toss anyway. The purchase already happened, so the reward is pure upside.

These four apps turn receipts into rewards with almost no effort. Every one of them is free.

| # | Receipt app | Best for | Sign-up bonus | Join |

|---|---|---|---|---|

| 1 | Fetch Rewards | Any receipt, any store | $1.50 with code | Join Now |

| 2 | Swagbucks | Receipts plus surveys | $5 | Join Now |

| 3 | Pogo | Earning on autopilot | Varies | Join Now |

| 4 | Ibotta | Grocery offers | Varies | Join Now |

Fetch Rewards gives points on any receipt from any store, then converts them into gift cards. Bonus points stack when you buy featured brands you already like.

Snap the receipt within a few days of shopping and let the points quietly accumulate. The whole process takes about ten seconds per trip.

Link your email so digital receipts from online orders import automatically. That single setting captures rewards you would otherwise forget to claim.

Because it works on groceries, gas, and restaurants, the points add up faster than most people expect over a full year.

Points convert into gift cards for Amazon, Walmart, and dozens of other retailers. A steady scanner can bank $50 to $100 in cards across a single year.

8. Use Browser Cash-Back Extensions at Checkout

A free browser extension can apply coupons and cash back automatically while you shop. You do nothing but click “buy” as usual.

These are the extensions worth installing first. All of them are free and take one click to add.

| # | Extension | Best for | Get |

|---|---|---|---|

| 1 | TopCashback | Highest cash-back rates | Get It Free |

| 2 | Rakuten | Cash back while you shop | Get It Free |

| 3 | BeFrugal | Up to 40% back plus coupons | Get It Free |

| 4 | Honey | Coupons at 30,000+ sites | Get It Free |

TopCashback and similar tools scan for working promo codes and better prices right at checkout. When a code lands, the savings are instant and require zero effort.

Some extensions also add their own cash-back rewards on top of any code they find. That means you can save on the price and earn on the purchase at the same time.

Add it to both your laptop and your phone browser so no purchase slips through. Deals get missed most often on mobile, where nobody remembers to hunt for codes.

Install it once and forget it. The tool does the hunting every time you reach a checkout page.

Stick to well-reviewed extensions from a company you actually recognize, since a sketchy one can track your browsing. Trusted tools stay free by earning retailer commissions, not by selling your data.

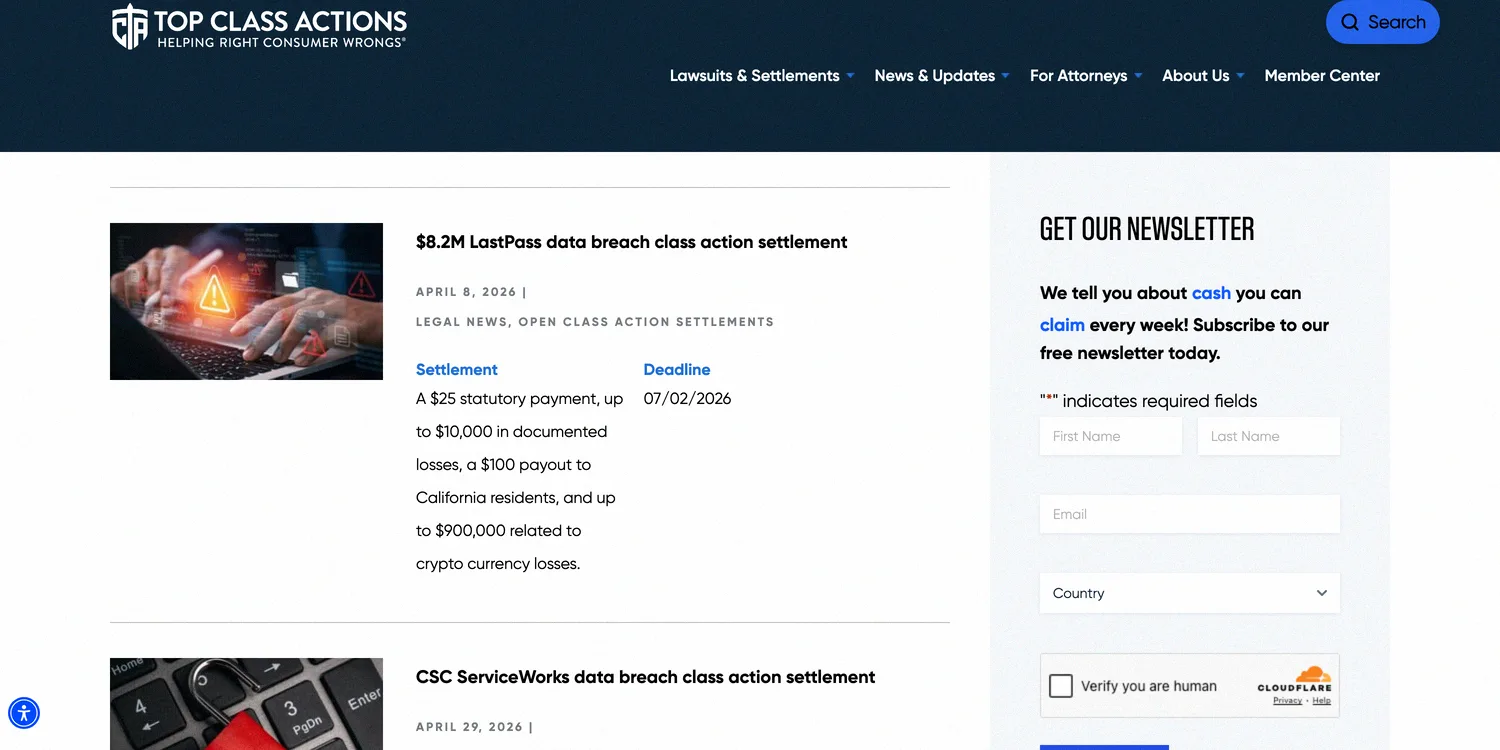

9. Claim Class-Action Settlement Payouts

When a company settles a lawsuit, everyday customers can claim a cash payout. You often qualify without ever knowing the case existed.

Top Class Actions is the easiest tracker to start with. Its open settlements page lists each case with the payout amount, the deadline, and a direct link to submit a claim.

Data breaches, false advertising, and hidden fees regularly end in settlements that pay affected buyers. Many only ask you to confirm you owned the product or used the service.

Sites that track open settlements list the deadlines and eligibility rules in plain English. Filing usually takes a few minutes, and smaller claims often need no proof of purchase.

Bookmark a settlement tracker and check it once a month. New cases open constantly, and each missed deadline is money left behind.

Payouts range from a few dollars to a few hundred, and they arrive by check or PayPal months later. Set a reminder and treat each one as a surprise deposit down the road.

Recent data-breach settlements have paid customers anywhere from $25 to over $100 for a two-minute claim. You attest under penalty of perjury, though, so only file for cases that genuinely apply to you.

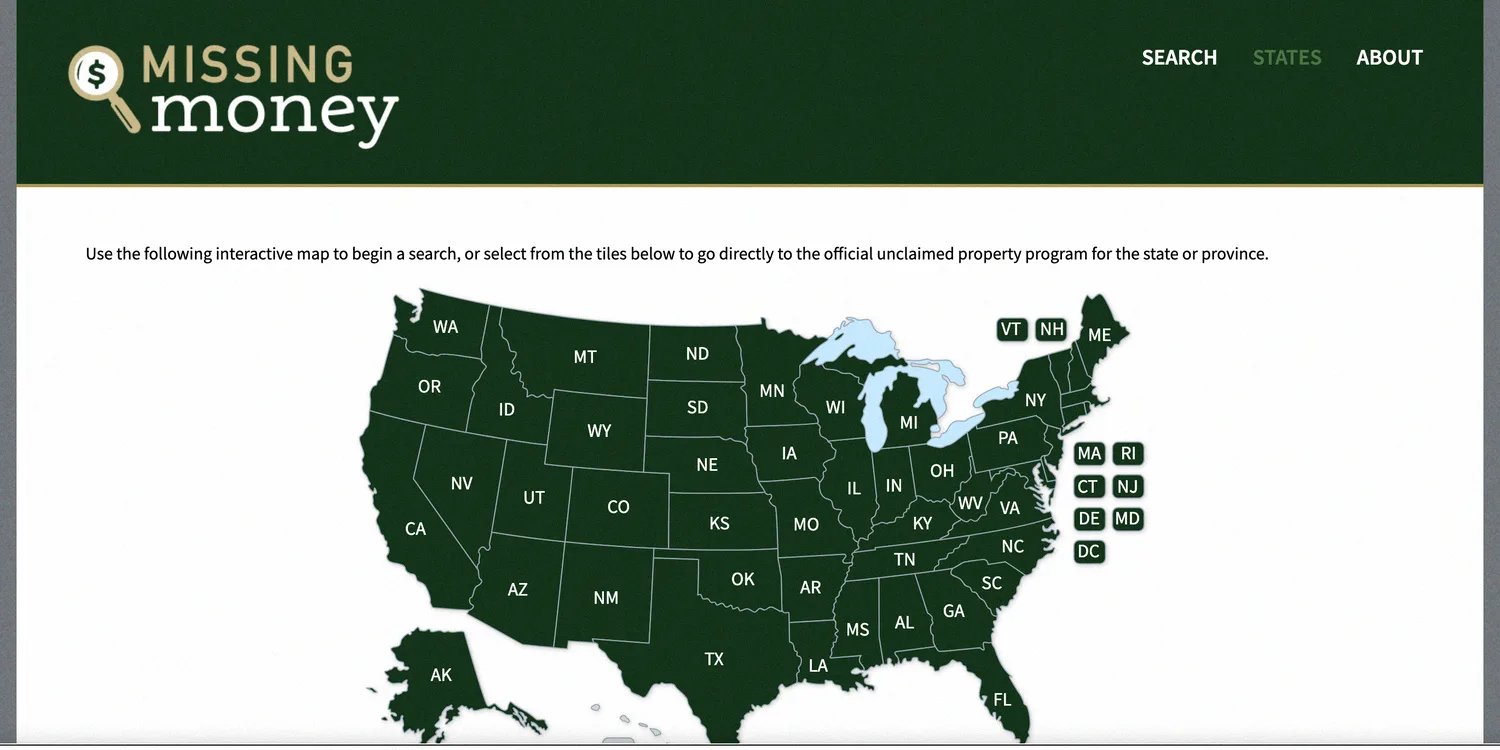

10. Search for Unclaimed Money in Your Name

This is money that is already yours. States hold billions in unclaimed property, sometimes called found money, in the form of forgotten paychecks, deposits, refunds, and insurance payouts.

Search your name for free at MissingMoney.com and your state treasurer’s unclaimed property site. Check every state you have ever lived in, along with former spouses, maiden names, and deceased relatives you may inherit from.

Old bank accounts, utility deposits, and uncashed checks all end up with the state after a few years of inactivity. The government then legally has to give it back the moment you ask for it.

My own search turned up $214 from that utility deposit I mentioned earlier, one I forgot I ever paid. The state mailed the check about five weeks after I filed the claim.

Claims are always free to file, so never pay a “finder” who offers to recover it for a cut of the total. Those middlemen just run the exact same free search, then bill you for the privilege.

The average claim runs a few hundred dollars, but five-figure payouts happen more often than you’d think. Set a reminder to run the search again once a year, since new funds get turned over to the state constantly.

Life insurance benefits, tax refunds, and old security deposits are the most common buckets. The official database is backed by state treasurers, so a paid recovery service adds nothing but a fee.

11. Cash In on Referral Bonuses

Referral programs pay you to recommend apps you already use and like. Both you and your friend usually pocket cash or account credit.

These referral programs pay the most reliably right now, and each link takes seconds to share.

| # | Program | Referral bonus | Join |

|---|---|---|---|

| 1 | Rakuten | $50 per friend | Join Now |

| 2 | Swagbucks | 10% of friend's earnings | Join Now |

| 3 | Fetch Rewards | Varies by promo | Join Now |

Banks, cash-back apps, food delivery services, and brokerages nearly all run refer-a-friend offers. A single share can be worth $5 to $50, and a few active friends add up quickly.

Post your link where it genuinely helps, like a group chat planning a grocery run or a friend asking for app suggestions. Spamming strangers rarely converts and can get your account banned.

Keep your best-paying referral links saved in your notes app for easy sharing. That way, when someone asks for a recommendation, you’re ready to send it in seconds.

Bank referrals tend to pay the most, with some refer-a-friend bank bonuses worth $50 to $100 for every friend who signs up.

Some programs cap how many friends you can refer each year, so read the fine print before you go wide. Focus your energy on the two or three offers that actually pay the most.

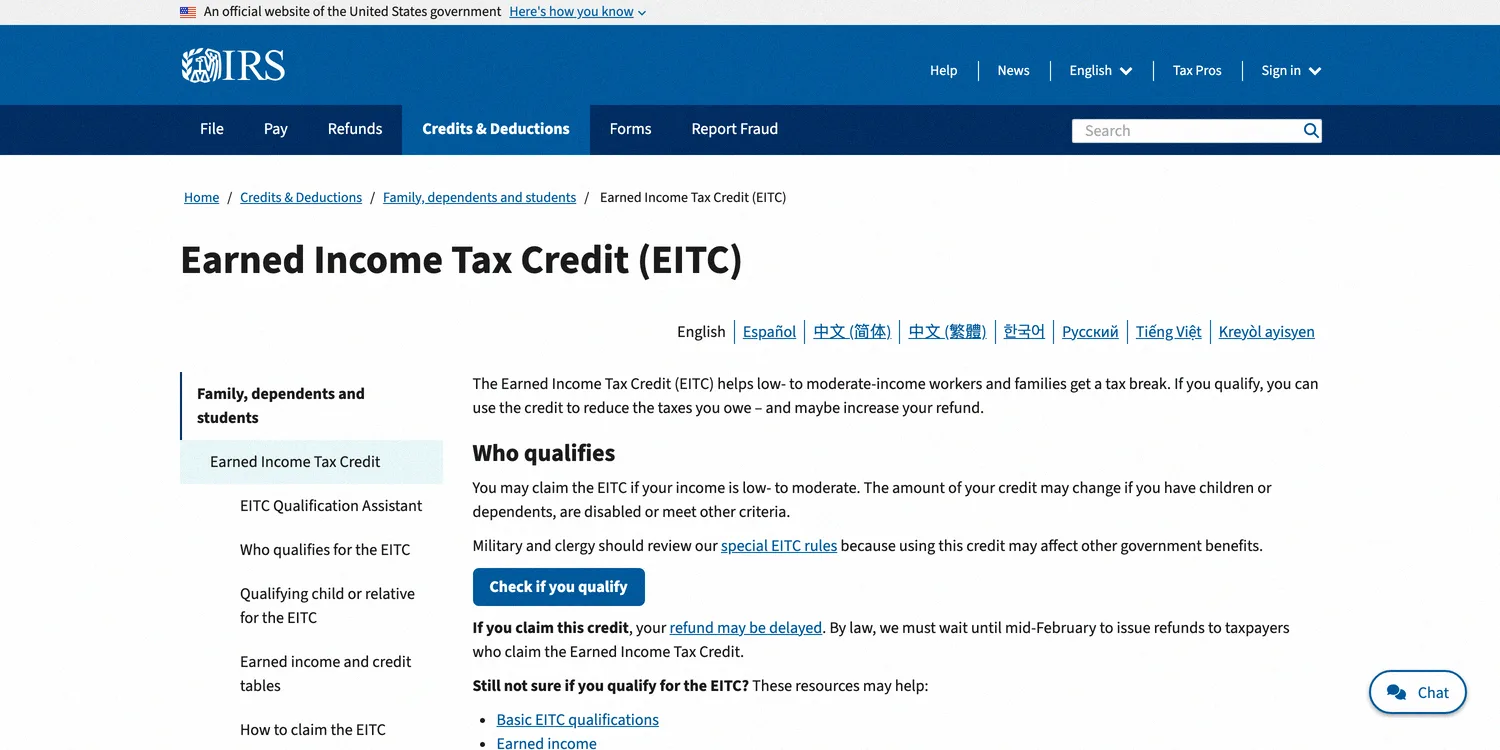

12. Tap Free Government Money and Assistance Programs

Federal and state programs give out real money that never has to be repaid. Grants, tax credits, and utility assistance are all technically free money.

The Earned Income Tax Credit alone returns thousands to eligible workers, yet many people who qualify never claim it. Energy assistance, childcare subsidies, and down-payment grants add even more on top.

Start at Benefits.gov to screen for programs you may already qualify for. The check-list takes a few minutes and never asks you for payment.

Re-check your eligibility whenever your income or family size changes. A new baby, a job loss, or a move can open programs that were closed to you last year.

Plenty of no-repayment government programs hand out grants and credits that you never have to pay back.

Options like LIHEAP for energy bills, SNAP for groceries, and WIC for young families all put money or benefits back in your hands. None of them ask for a single cent in repayment.

13. Claim Employer Perks and FSA Money You Are Leaving Behind

Your job likely offers free money in benefits you never bothered to activate. Wellness bonuses, tuition help, and account matches often go completely unused.

Many employers pay a cash wellness incentive for a health screening or gym visit. Others match charitable gifts or offer discounted stock through an employee purchase plan.

Check whether you have a Flexible Spending Account balance that expires at year-end. That’s your own pre-tax money, and letting it vanish is the opposite of a hack.

Ask HR directly for the full benefits guide rather than skimming the enrollment portal. The most valuable perks are often the ones nobody advertises.

Read your benefits summary once a year with a highlighter in hand. Most people find at least one perk worth real money that they had forgotten they had.

A Health Savings Account works similarly but rolls over every year, and some employers seed it with free cash. Tuition reimbursement can add a few thousand more if your workplace offers it.

14. Unlock Free Money for Students

Students have access to free cash that disappears the moment you graduate. Grants, campus perks, and buyback programs all count toward it.

Federal Pell Grants and school-specific scholarships hand out money that never needs repayment, yet billions go unclaimed each year. Filing the FAFSA is the first step and costs nothing.

Beyond aid, sell used textbooks through buyback sites like BookScouter and lean on free student software and streaming discounts. Every dollar you do not spend is a dollar earned.

Ask your department about small scholarships and stipends that few students apply for. Tiny, low-competition awards are some of the easiest free money on any campus.

Amazon Prime Student, free Microsoft and Adobe tools, and a simple library card all cut costs to near zero. Student discounts on software and streaming quietly save hundreds over a full degree.

Side income helps too, and the best online jobs for students are flexible enough to fit around a class schedule.

15. Move Idle Cash to a High-Yield Savings Account

Money sitting in a standard account is quietly losing value, while a high-yield account pays you to hold it. The interest is free money for doing absolutely nothing.

Here are the rates the big online banks are paying right now. Rates change often, so confirm on the bank’s site before you open.

| # | Bank | Account | APY right now | View |

|---|---|---|---|---|

| 1 | SoFi | Checking & Savings | Up to 3.80% | View Rates |

| 2 | Ally | Online Savings | 3.00% | View Rates |

| 3 | Capital One | 360 Performance Savings | 3.00% | View Rates |

Traditional big-bank savings accounts pay almost nothing, while top online banks pay far more on the exact same balance. On a $5,000 emergency fund, that difference can be a couple hundred dollars a year.

Moving my own emergency fund over took one evening, and it now pays me around $15 in interest every month. That same balance used to earn about 40 cents at my old big bank.

Opening an online high-yield account takes about ten minutes, and your money stays FDIC-insured the whole time. There are no fees and no lock-up on most accounts.

Set up an automatic transfer so every spare dollar quietly earns while you sleep. It’s easily the most passive hack on this entire list.

Top online banks currently pay around 3% to 4% APY, while many big banks pay a tiny fraction of that. On the same balance, that spread is pure free money for ten minutes of switching.

How to Stack These Hacks for the Biggest Payout

The real magic happens when you combine hacks instead of running them one at a time. Layering a few together multiplies the return on a single purchase or paycheck.

Picture buying groceries with a rewards credit card, through a cash-back app, using a store sale, and scanning the receipt afterward. That one trip can trigger four separate payouts at once.

Start with the set-and-forget hacks like your 401(k) match and a high-yield savings account. From there, layer the active ones like sign-up bonuses and cash-back apps on top over the following weeks.

Give yourself one “money admin” hour a month to claim bonuses, cash out apps, and check for new settlements. That single hour is often the best-paid hour of the entire month.

How Much Free Money Can You Actually Collect?

Stacked over a single year, these hacks add up to far more than most people expect. Here’s a realistic running total for someone who works the list without chasing anything exotic.

| # | Free money source | Realistic first-year value |

|---|---|---|

| 1 | Full 401(k) match | $2,000 to $3,300 |

| 2 | Bank + credit card bonuses | $400 to $900 |

| 3 | Cash-back and receipt apps | $300 to $600 |

| 4 | Unclaimed money claim | $0 to $500+ |

| 5 | High-yield savings interest | $150 to $250 |

| 6 | Surveys, free stock, settlements | $150 to $400 |

Add it up and a motivated household clears roughly $3,000 to $5,000 in the first year. The recurring hacks then keep paying every year after that, with almost no extra effort on your part.

How to Spot a Free Money Scam

Real free money has one thing in common: you never pay to get it. That single rule filters out almost every scam you’ll ever run into.

Walk away the moment an offer asks for an upfront fee, a gift-card payment, or your full Social Security number over the phone. Legitimate programs, banks, and settlements never operate that way.

Be extra cautious with “instant $1,000” ads and messages promising huge payouts for no effort. Those funnels usually harvest your data or push endless paid offers that never actually pay out.

Stick to official sites like your state treasury, Benefits.gov, and known bank and brokerage apps. When an offer sounds too good, verify it directly with the source before handing over a single detail.

FAQ

How can I get money for free right now?

The fastest options are claiming a free stock from a brokerage sign-up, redeeming a cash-back or survey app balance to PayPal, and searching MissingMoney.com for unclaimed cash. Free stock and app cash-outs can hit your account within minutes to a few days.

How can I get $1,000 right now?

No single hack pays $1,000 instantly, but stacking several gets you there fast. A bank sign-up bonus, a credit card welcome bonus, and a decent unclaimed-money claim can each contribute a few hundred dollars, and a full 401(k) match adds thousands over the year.

Are free money apps legit?

Many are, including established names like Rakuten, Ibotta, Fetch Rewards, and Swagbucks. The safe rule is to use apps that pay you and never charge a fee, and to be skeptical of any app promising huge instant payouts for no effort.

What is the fastest free money hack on this list?

Free stock offers and cash-back app cash-outs pay quickest, often the same day. Unclaimed money is the largest low-effort payout, but it can take a few weeks to process.

What’s the best free money hack to start with?

Start with your full 401(k) match if you have one, since it’s guaranteed money at an instant 50% to 100% return. If you don’t, run a free unclaimed-money search and open a high-yield savings account first.

Is there an app that gives you free money?

Several legit apps pay real cash, including Rakuten and Ibotta for cash back, Swagbucks and Survey Junkie for surveys, and Fetch Rewards for scanning receipts. None charge a fee, and most pay out through PayPal or gift cards once you hit a low threshold.

Is unclaimed money really free?

Yes, unclaimed money is your own forgotten cash that a business turned over to the state. Claiming it is always free through official state sites, so never pay a recovery service to retrieve it for you.

Jason is a personal finance expert and the founder of Frugal For Less. He has spent over a decade researching and testing hundreds of money-making apps, survey sites, and savings strategies to help readers earn more and keep more of their hard-earned cash.

More about the author →

Want to learn how to make an extra $1,000 per month?

Download our free guide with:

- 10 Side Hustles to Make $1,000/month

- Worksheet for setting money making goals

- Resource List to help you succeed